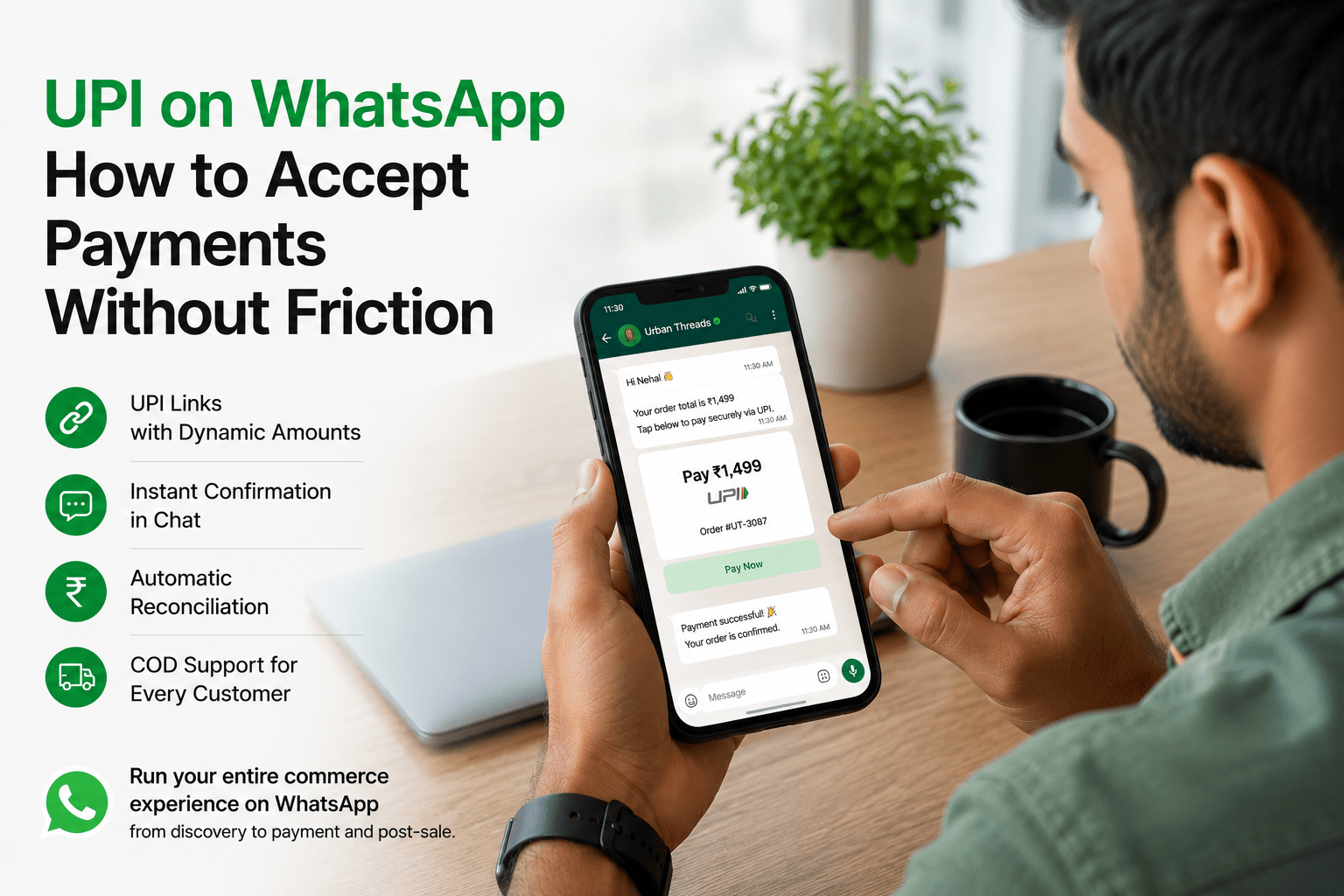

UPI is what makes WhatsApp commerce work in India.

It removes the single biggest source of drop-off in any online checkout - entering card details, OTPs, billing addresses, and waiting for verification. With UPI, the customer authorises a payment from their UPI app in a few taps, and the merchant has the money within seconds.

Doing this inside a WhatsApp conversation, without the customer leaving the chat, is the goal of every well-built Indian WhatsApp commerce setup. Here is how the actual implementation choices work.

Three ways to accept UPI on WhatsApp

1. UPI link (most common)

Your automation platform generates a UPI payment link with the merchant ID, amount, and order reference. The customer clicks the link, their UPI app opens (Google Pay, PhonePe, Paytm, BHIM, others), payment is confirmed, the app returns to WhatsApp.

Pros - works for every UPI user, no platform-specific dependencies, mature implementation across BSPs and automation platforms, supports both static and dynamic amounts.

Cons - the customer briefly leaves WhatsApp. Some customers drop off here, especially first-time customers who are not sure what is happening.

2. Payment gateway link

A payment gateway (Razorpay, Cashfree, PayU, others) generates a hosted payment page that supports UPI, cards, netbanking, and wallets. The customer clicks the link, picks a payment method, completes payment, returns to WhatsApp.

Pros - supports payment methods beyond UPI (helpful for COD-averse Tier 1 customers who prefer cards), unified reconciliation, more sophisticated retry and recovery logic on the gateway side.

Cons - adds a step compared to direct UPI link, payment gateway fee per transaction.

3. WhatsApp Pay (in-app UPI)

Meta's native UPI payment feature inside WhatsApp. Payment authorisation happens entirely inside the chat, no app switch.

Pros - smoothest possible flow, customer never leaves WhatsApp.

Cons - measured rollout in India, not yet universally available across all customer accounts, fewer integration paths than the alternatives, and lower share of transactions than the link-based methods today.

Most large Indian retailers today use a combination - UPI link as the default, payment gateway link for larger orders or for non-UPI payment options, WhatsApp Pay where available and preferred.

What reduces friction in practice

Dynamic amounts

The payment link should auto-populate the exact order amount. Asking the customer to type the amount is a drop-off point and a risk.

Order reference in the payment

The order reference should be embedded so reconciliation is automatic. Manual matching of orders to payments costs staff time and creates errors.

Immediate confirmation back to the chat

Once payment is received, an order confirmation should land in WhatsApp within seconds. Webhook-based confirmation back from the gateway to your automation platform makes this possible.

Failed payment recovery

Payments fail. UPI apps time out. Bank servers go down for maintenance. The customer should not be left wondering what happened. A failed payment should trigger a retry message in chat with a fresh link.

Cash on delivery - still relevant

For Tier 2 and Tier 3 customers, COD often outperforms UPI in trust and conversion - especially for first-time buyers.

WhatsApp commerce should support COD as a payment option in the checkout flow. The order proceeds without a payment step. Logistics collects on delivery. Reconciliation flows back through the logistics partner's COD settlement.

The mistake - treating COD as a degraded option. For a meaningful share of the Indian market, COD is the preferred option and conversion goes up when it is offered prominently.

Reconciliation - the back-office work most setups underbuild

Payments need to flow back into the order management system, accounting system, and tax records.

Done well - payment webhook from gateway hits the automation platform, which updates the order status, marks the order as paid in the order management system, generates the GST-compliant invoice, and triggers the dispatch workflow.

Done badly - payments land in a payment gateway dashboard, orders sit in a chat dashboard, and someone manually matches them at end of day. Mistakes compound, GST filings get messy, and refunds become a nightmare to trace.

The shift to make

Stop treating payment on WhatsApp as 'send a UPI ID and ask for proof of payment.'

Start treating it as a fully integrated payment flow - dynamic link, immediate confirmation, automatic reconciliation, fallback options for failed payments, and COD support for customers who prefer it.

Payment is where most WhatsApp commerce setups in India quietly lose value. Fixing payment alone typically improves conversion noticeably and reduces back-office cost meaningfully.

About the Author

Avni Chadha

Ready to orchestrate your AI future?

Converiqo AI helps you design, deploy, and scale automation workflows that move your business faster, leveraging specialized solutions like our AI bot platform for lead generation, customer self-service AI bot platform, employee self-service AI bot platform, retail omnichannel automation, and our detailed guides on how agentic AI bot platforms work in enterprises and cost structure of enterprise AI bot platforms. Connect with our team to see the platform in action and co-create the next chapter of intelligent operations.

Read More Blogs

Discover more insights and product updates curated by the Converiqo AI team.

Real ROI of Field Force Automation - Beyond the Activity Dashboard

Four metrics that show real field force automation ROI in India - productivity, data reliability, throughput, and field attrition - not just the activity dashboard.

Beat Planning Is the Highest-Leverage Field Force Capability - Here Is Why

Beat planning decides coverage, call frequency, and whether field time is productive. Why it is the single highest-leverage field force automation capability.

Why an Indian Field Force App Has to Work Offline - and Be Built for Real Devices

Field work in India happens where connectivity is intermittent. A field force app that assumes constant connectivity fails exactly where field work is done.