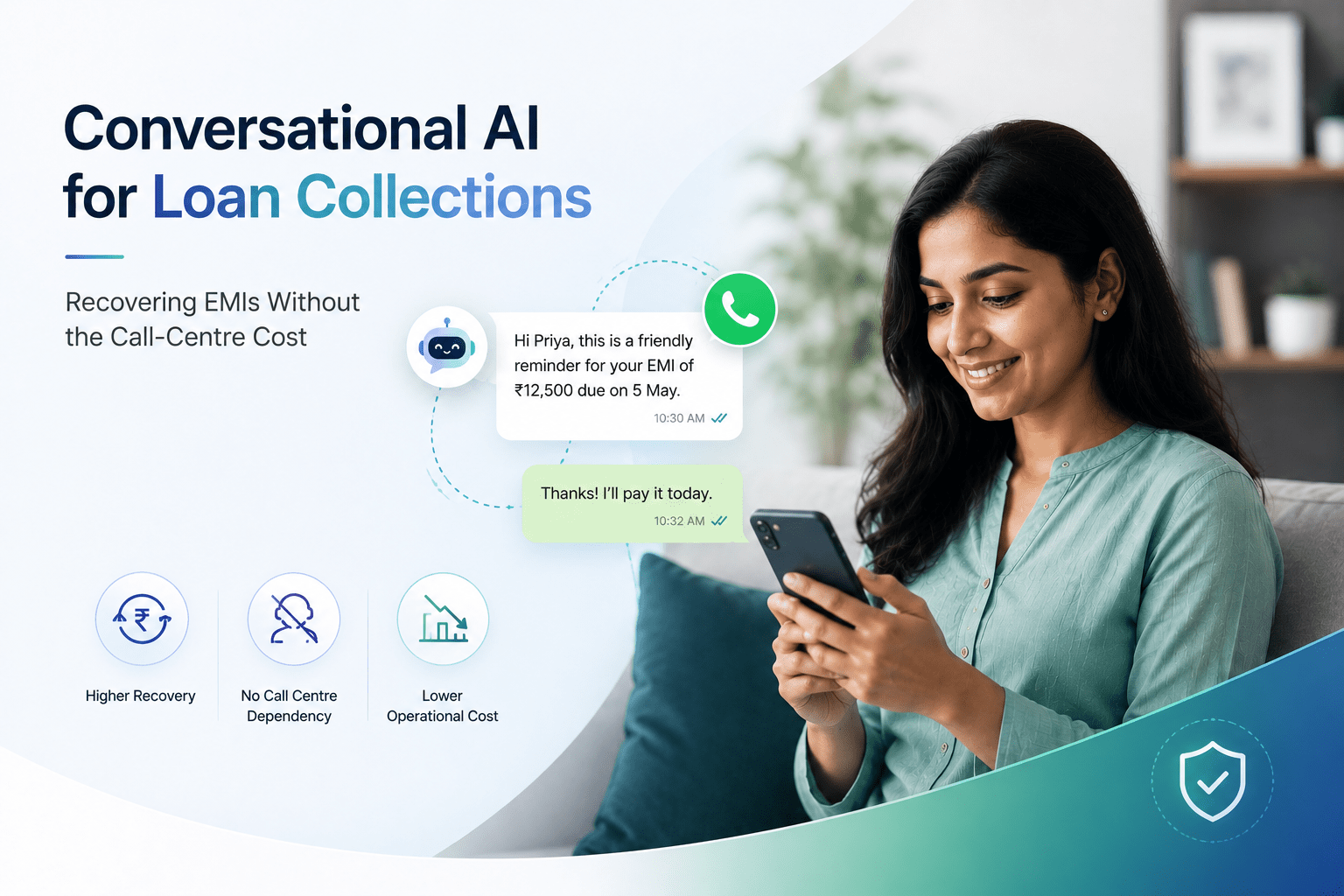

Collections is the part of lending no one enjoys and every lender depends on. For NBFCs and banks alike, the early-stage collections operation - the reminders and follow-ups around EMI due dates - is expensive to run, hard to scale, inconsistent in quality, and a frequent source of friction with customers the lender would rather keep. Conversational AI changes the economics of this work more quietly, and more profoundly, than almost any other BFSI use case.

Why traditional early-stage collections is so costly

The conventional model leans on outbound calling. Calling is expensive per contact and does not scale smoothly - more borrowers means more agents, more training, more management. It is inconsistent: outcomes and tone vary from agent to agent and call to call. Much of the effort is wasted on contact attempts that never connect. And it carries relationship risk: a poorly handled collections call can damage, sometimes permanently, the standing of a customer who simply forgot or was briefly short. For early-stage cases - borrowers who are not wilful defaulters but ordinary people who missed a date - that risk is disproportionate to the situation.

What conversational AI does differently

A conversational agent on WhatsApp reframes early-stage collections as a service interaction rather than a confrontation.

-

Timely, gentle reminders - a clear, polite message before and around the due date, when a nudge is most likely to simply work.

-

A payment path inside the message - the reminder carries the means to act, so paying is one tap away rather than a separate errand the borrower has to remember.

-

Consistency at any scale - every borrower receives the same correct, respectful, compliant communication, whether the book is ten thousand accounts or ten lakh.

-

Genuine two-way dialogue - a borrower can reply, ask about the amount or date, or raise a difficulty, and the agent responds rather than only broadcasting.

-

Intelligent escalation - cases that need human judgement, or that signal genuine hardship, are routed to a trained officer with the full context already assembled.

The relationship argument

The instinct is to frame collections automation as pure cost reduction, and the cost reduction is real and large. But the relationship effect may matter as much. Most early-stage delinquency is not wilful - it is a missed date, a temporary cash gap, an oversight. Meeting that customer with a respectful, helpful, easy reminder rather than a pressured call recovers the money and preserves the relationship. That customer can be retained, served, and responsibly cross-sold to for years. A collections process that recovers the EMI but loses the customer has won a battle and lost the war.

The compliance imperative

Collections communication is rightly held to fair-practice standards. This is an area where conversational AI, designed well, is an advantage rather than a risk. Every message is consistent, on-template, on-record and reviewable - there is no variability of an individual agent having a bad day. Communication stays respectful and non-coercive by design. Frequency and timing are controlled. And every interaction is logged and auditable. Designed around fair-conduct principles and validated with the lender's compliance team, an automated collections agent can be more consistently compliant than a human calling floor, not less. The deployment must, of course, be built to current regulation for digital lending and customer communication - compliance is a design input here, not an afterthought.

Where to begin

Early-stage, pre-due and just-past-due reminders are the natural starting point: the highest volume, the most repetitive, the least sensitive, and the place where a timely nudge does most of the work on its own. Get that flow genuinely right - integrated with the loan management system, compliant, resolving with a payment path, escalating hardship cleanly - and a lender has both a measurable result and the foundation to extend conversational AI across the rest of the collections journey. The pillar article this supports places collections within the full BFSI conversational-AI picture.

About the Author

Yash Soni

Ready to orchestrate your AI future?

Converiqo AI helps you design, deploy, and scale automation workflows that move your business faster, leveraging specialized solutions like our AI bot platform for lead generation, customer self-service AI bot platform, employee self-service AI bot platform, retail omnichannel automation, and our detailed guides on how agentic AI bot platforms work in enterprises and cost structure of enterprise AI bot platforms. Connect with our team to see the platform in action and co-create the next chapter of intelligent operations.

Read More Blogs

Discover more insights and product updates curated by the Converiqo AI team.

Real ROI of Field Force Automation - Beyond the Activity Dashboard

Four metrics that show real field force automation ROI in India - productivity, data reliability, throughput, and field attrition - not just the activity dashboard.

Beat Planning Is the Highest-Leverage Field Force Capability - Here Is Why

Beat planning decides coverage, call frequency, and whether field time is productive. Why it is the single highest-leverage field force automation capability.

Why an Indian Field Force App Has to Work Offline - and Be Built for Real Devices

Field work in India happens where connectivity is intermittent. A field force app that assumes constant connectivity fails exactly where field work is done.